Saturday, March 25, 2017

Tuesday, January 31, 2017

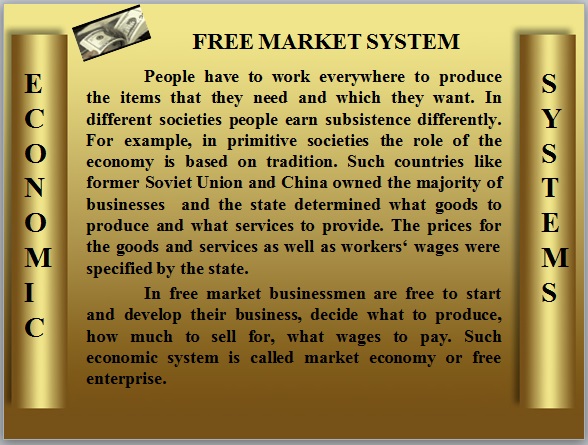

In Lithuania --> The initial business plan

Step forward!

Students’ Training Company (STC)

Students’ Training Company (STC)

The

initial business plan

- What is your product or service?

----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

- Who will be the most interested

in buying your product or service? (Ex. Your school students, people who

love cooking, families having CD players, football fans, etc.)----------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------------

- How much do you think these

people will pay for your product or service? -------------------------------Where

do you know this from? (Ex. „It’s as much as I would pay myself”, „I asked

my mother and several of her friends” and “Similar product in the music

shop costs 0.60 Euros more”). ----------------------------------------------------------------------------------------------------------------------------------------

- GREAT QUESTION. Will your price

cover the costs of materials, labour and costs of your company? ------------------------------------------------------------------------------------------------------------

- What are the costs of all

materials? (Ask your teacher or consultant). ---------------------------------------------------------------------------------------------------------------------------------------------------------------

These are the costs for

purchasing materials.

- Does your price cover the costs

of one material? -------------------Yes-----------------------No.

If not. You would rather

look at the current price. Otherwise, your company will suffer loss! If so,

will the price cover other costs? It is difficult to answer this question

without detailed information. However, if you follow the following guidelines,

your company will cover the costs of other materials, labour and activities.

Materials costs (€) Retail price (€)

1.00

2.00

3.00 5.00

5.00 8.00

10.00

15.00

- Based on this information, what

price do you offer? ----------------------------------------------------------------------------------------------------------------------------------------------------------------------------

- Almost everything is done! Now

you have to set the task of producing and sales. You surely have to sell

more than one product. What is the difference between the prices of

product and the price of material costs (See previous paragraph 4B)? -----------

How many products will the company have to sell to cover the costs of all

materials (See 4A) ------------ In order to sell all the costs multiply

that number by 1.5. The resulting figure will be the target of your

production and sales. Can these tasks be fulfilled? How many products or

services will every member of the company have to sell? ---------------------------------------------------------------------------------------------------------------------------

- Summarize your plan. We expect

to produce and sell------------ products or services by-----------------

(date) for -----------€ each (including

taxes).

Product

Pricing Sheet

STEP I. IDENTIFY YOUR COMPANY’S

FIXED COSTS.

Your company’s fixed costs are the

costs, which remain the same no matter how many products you produce. The

example below shows what the usual fixed costs of students’ training companies are.

It suits for the company with 15 members and which works for 15 weeks.

No.

|

Costs

|

An example company

|

Your company

|

1.

|

Earnings -10*0,80 € per hour

|

208€

|

€

|

2.

|

Wages

|

182.00€

|

|

3.

|

Rent

|

10.00€

|

|

4.

|

Stationery goods

|

8.00€

|

|

5.

|

Tools, equipment

|

10.00€

|

I

|

6.

|

Marketing costs

|

10.00€

|

|

7.

|

The fee for permission to start

|

40.00€

|

|

8.

|

Bank services

|

5.00€

|

|

9.

|

Insurance

|

5.00€

|

|

10.

|

Annual report

|

10.00€

|

|

11.

|

Small costs

|

10.90€

|

|

Total fixed costs

|

498.90€

|

Note.

Earnings are actually variable costs. Earning costs usually vary when the

number of workers and the number of hours needed to produce the product vary.

If the demand of a product is growing and the company is increasing its

production, the labour costs increase as well. However, the company’s employees

are employed on a fixed number of hours. They are paid for the time spent in

company’s meetings and other activities. That is why the company’s earnings are treated

as fixed costs.

STEP II. IDENTIFY YOUR COMPANY’S VARIABLE COSTS.

If the company’s variable costs are the costs that vary depending on the

number of products or services provided,

Be sure to fill in a separate worksheet for each of your company’s

product or service.

Product: ---------------------------------------------------------------------------------------------------------------------

VARIABLE COSTS-------------------------------------------UNITS

No.

|

Select “Variable costs” estimated in your production plan

|

|

1.

|

The planned costs of materials purchased

|

€

|

2.

|

: Number of units

|

+

|

3.

|

= Material costs of a single product

|

= €

|

4.

|

* Bias waste, error, etc. (20%)

|

* 1,2 €

|

5.

|

= Revised one product materials

costs

|

= €

|

STEP III. IDENTIFY THE PRICE

OF A PRODUCT OR SERVICE.

Once you have rated the fixed and

variable costs of the main products, you can set the price, which will be

profitable for your company.

Product: ---------------------------------------------------------------------------------------------------------------------

The table below will help to

determine your gross profit per unit at various selected prices. Gross profit per unit is the difference

between the price and the design of a product and selling expenses.

Examine the example and consistently

follow the instructions.

CALCULATE THE GROSS PROFIT OF A UNIT WITH DIFFERENT PRICES

No.

|

The 1st

selected price

|

The 2nd

selected price

|

The price of the 1st

sample

|

The price of the 2nd

sample

|

|

1.

|

Retail price of a unit

|

5.19€

|

5.66€

|

||

2.

|

Commissions (minimum 10%)

|

-

|

-

|

0.52

|

0.57

|

3.

|

Retail price = commissions

|

=

|

=

|

= 4.67

|

= 5.09

|

4.

|

The revised costs of materials

for one unit

|

-

|

-

|

1.52

|

1.52

|

5.

|

= Gross profit per unit

|

=

|

=

|

= 3.15

|

= 3.57

|

Line 1. Select two control prices of your product. One price should be

‘big’ and the other ‘small’.

Line 2. Calculate the commissions for the sale, which will be paid at

the chosen price (Commission for sales must be at least 10%), and enter it into

this line. Subtract the commission from the chosen price and enter the result

into the 3rd line.

Line 3. Record the adjusted material costs of one product, which you calculated

in the 2nd step 5th

line. Subtract this amount from the amount in the 3rd line

and write down the result into the line 5.

Line 5. This is your gross profit of one unit – the difference between

the price of your product and selling expenses.

Wednesday, January 11, 2017

Subscribe to:

Posts (Atom)